Think It’s Better To Wait for a Recession Before You Move? Think Again — Especially Now.

Fear of a recession is back in the headlines — and this time, it’s layered with growing global tension. With the destruction of Irans nuclear facilities and the potential for military conflict rising, the global economy is facing more uncertainty. If conflict escalates into full-scale war, it could directly impact mortgage rates, inflation, consumer confidence, and ultimately the U.S. housing market.

A recent survey from John Burns Research and Consulting and Keeping Current Matters found that 68% of people are holding off on buying or selling due to economic uncertainty. And it’s not just fear. Many are waiting because they believe a downturn will make it more affordable to move. According to Realtor.com:

“In 2025 Q1, 3 in 10 (29.8%) surveyed homebuyers said a recession would make them at least somewhat more likely to purchase a home . . . This reflects a common dynamic where some buyers see a downturn as an opportunity.”

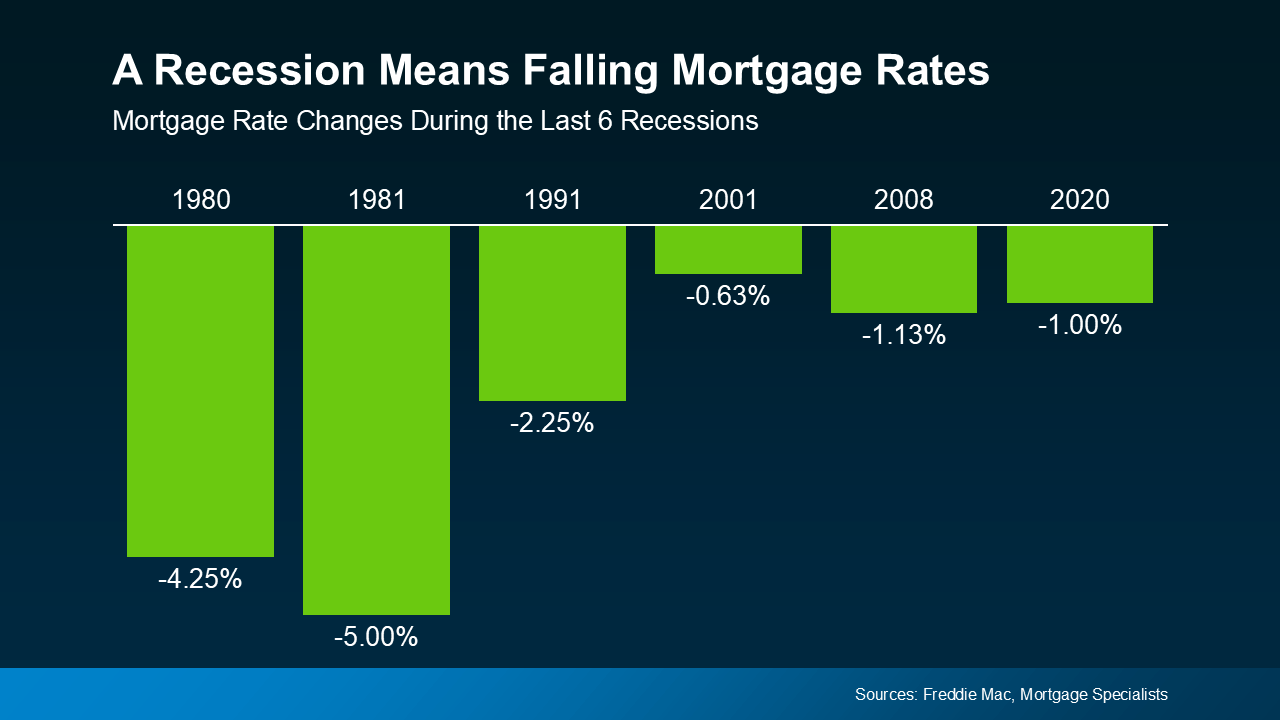

They’re hoping that a recession will cause the Federal Reserve to cut interest rates, making homes more affordable. And historically, that’s a reasonable assumption — mortgage rates tend to fall during recessions (see data from the last six downturns).

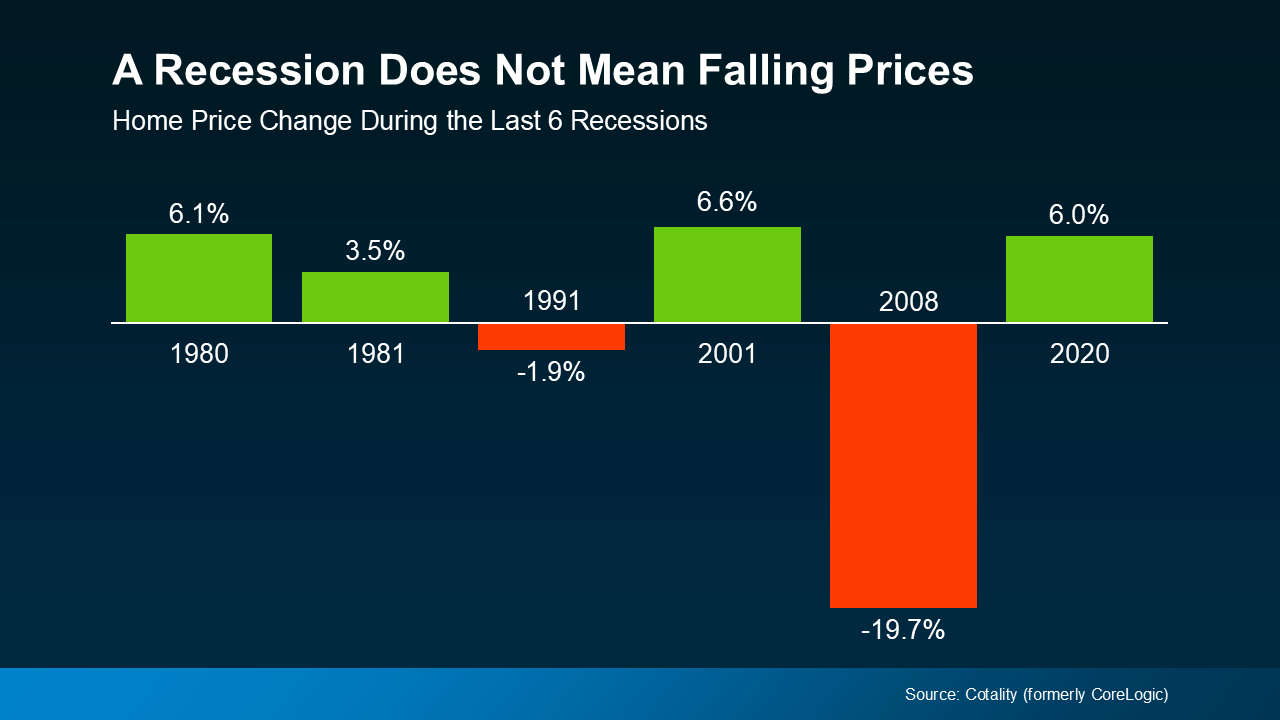

But here’s what those hopeful buyers may be missing: home prices don’t usually fall during recessions. According to data from Cotality (formerly CoreLogic), home prices rose in four of the last six. The only major drop was during the 2008 housing crisis — which was caused by risky lending and oversupply, not a typical economic downturn.

Now Add Geopolitics: What Happens If War Breaks Out with Iran?

If a war involving Iran erupts — especially one that disrupts global oil supply — the effects could ripple through the U.S. housing market in complex ways:

1. Mortgage Rates Could Fall... Temporarily

Global conflicts often trigger a “flight to safety,” meaning investors move money into U.S. Treasury bonds, driving yields down — and pulling mortgage rates lower along with them. But if oil prices spike due to war, that could increase inflation, which might pressure the Fed to pause or reverse any planned rate cuts — sending mortgage rates back up.

2. Higher Oil Prices = Higher Costs

War in Iran could likely send oil prices soaring, which impacts:

-

Transportation costs for construction materials

-

Utility bills for homeowners

-

The overall cost of living

That inflation pressure can weigh down buyer affordability and slow homebuilding.

3. Consumer Caution

In times of uncertainty, buyers and sellers may pause big decisions, especially first-time buyers or those in sectors impacted by inflation or market volatility.

4. U.S. Real Estate as a Safe Haven

Interestingly, turmoil abroad often boosts interest in U.S. real estate. Global investors and well-capitalized buyers may turn to stable cities — like those in the D.C. metro — as safe places to park their wealth. This can keep demand strong, even when domestic confidence wavers.

When Will Rates Come Down?

Most experts currently expect gradual interest rate cuts beginning in late 2025, depending on how inflation behaves and whether the economy slows down — or is further shaken by international conflict. But any escalation in the Middle East could delay those cuts or make rate movement more volatile.

The Bottom Line

If you’re waiting for a recession or a geopolitical event to give you the “perfect” conditions to buy or sell — you might be waiting on a market that never fully delivers what you're hoping for.

Yes, mortgage rates could come down.

No, home prices aren’t likely to follow.

And in the case of global instability, markets can move quickly in both directions — including higher rates, construction slowdowns, and buyer hesitation.

If you're thinking about making a move, let’s talk now — while you still have control, clarity, and opportunity. Together, we’ll build a plan that works regardless of what the headlines say.