Think a Fed Rate Cut Will Save Mortgage Rates? Think Again.

With the Fed expected to cut interest rates in September, a lot of people are hoping that mortgage rates will finally come down too. Buyers want relief, homeowners are wondering if refinancing will make sense, and investors are watching closely to see what happens next.

But here’s the key thing: a Fed rate cut doesn’t automatically mean mortgage rates will drop. In fact, there are a few reasons why they might stay high—or even move higher. Let’s dig in.

1. Mortgage Rates Don’t Follow the Fed Directly

This is one of the most common misconceptions in real estate. People assume that if the Fed cuts rates, mortgage rates instantly go down too. But that’s not how it works.

-

The Fed sets the federal funds rate, which is what banks charge each other for short-term loans.

-

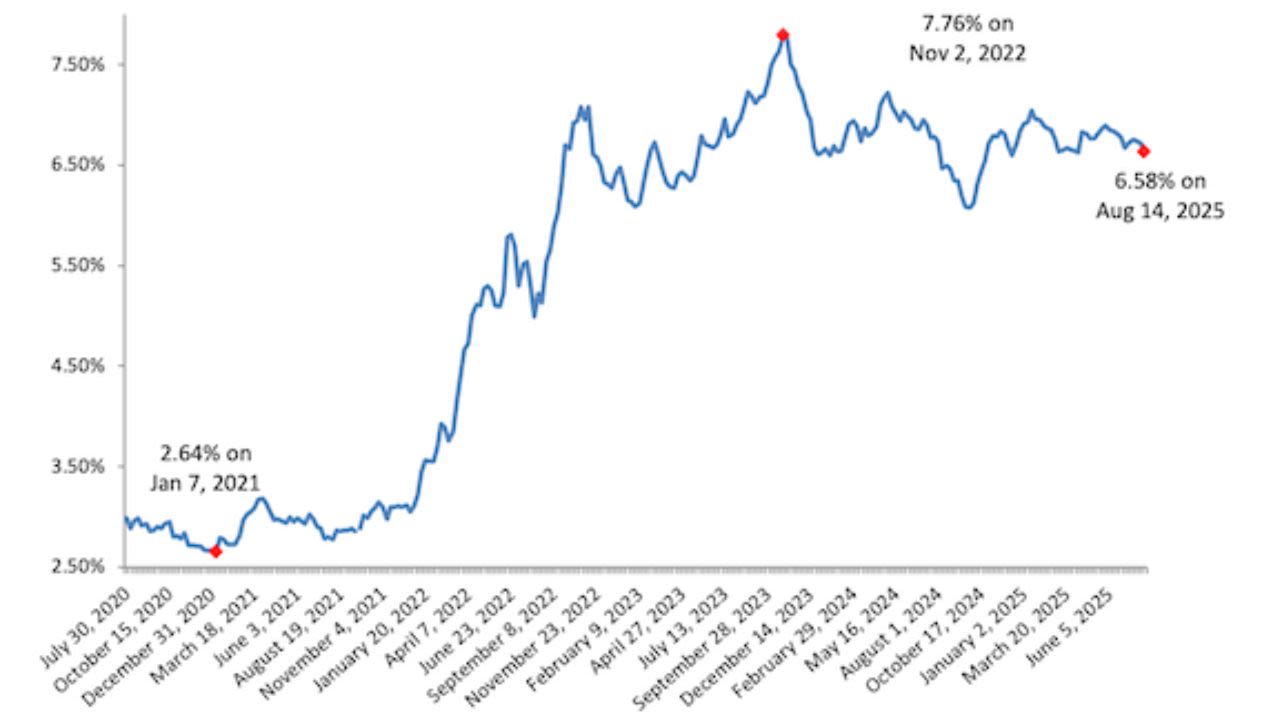

Mortgage rates, however, are tied more closely to the 10-year U.S. Treasury yield, which is a long-term bond.

Here’s why that matters: mortgage lenders look at the bond market to set rates. If investors believe that inflation will rise or the economy could face instability, long-term bond yields may go up. And when bond yields rise, so do mortgage rates.

So even if the Fed lowers short-term rates, the bond market may respond in a way that keeps mortgage rates flat—or even pushes them higher.

2. Markets May Have Already “Priced It In”

Another big factor is timing. Financial markets don’t wait around for the Fed to make an official announcement—they move ahead of time based on expectations.

This is called “pricing in.”

Here’s how it works:

-

If most investors already believe the Fed is going to cut rates in September, they’ve already shifted bond yields lower in anticipation.

-

That means when the Fed actually makes the cut, it won’t be a surprise.

-

And if it’s not a surprise, mortgage rates may not move much at all.

It’s kind of like when everyone already knows the ending of a movie before you watch it—by the time you see it, it’s not exciting anymore.

So if you’re waiting for September thinking rates will suddenly drop, don’t count on it.

3. Inflation Is Still the Big Player

The biggest reason mortgage rates are still high is inflation. Even after the Fed has raised rates aggressively to try to cool it, inflation hasn’t gone away.

-

Housing costs remain elevated.

-

Wages are still rising in many sectors.

-

Everyday essentials—from food to gas—remain sticky in price.

When inflation is high, investors demand higher returns on bonds to protect their money from losing value over time. That’s why Treasury yields stay elevated. And since mortgage rates are tied to Treasury yields, they remain high as well.

So until inflation is clearly under control, don’t expect mortgage rates to drop significantly—no matter what the Fed does.

4. The Bigger Picture Matters More Than the Fed

Here’s another layer: mortgage rates aren’t just about what the Fed says—they reflect the overall health of the economy.

Think about it this way:

-

If the Fed cuts rates because they’re worried the economy is slowing, that’s not exactly a sign of strength.

-

Investors might respond by becoming more cautious, asking for higher yields to protect themselves from future risks.

-

Lenders may also hesitate to lower mortgage rates if they fear an increase in defaults or weaker housing demand.

So ironically, a rate cut meant to help the economy could actually keep mortgage rates from falling if it sends the signal that we’re heading toward trouble.

5. Don’t Forget Global Factors

Lastly, mortgage rates don’t exist in a vacuum. The U.S. economy is deeply connected to the global market, and international trends also influence where rates go.

For example:

-

If there’s geopolitical instability (like conflicts abroad), investors might move money differently.

-

If foreign demand for U.S. Treasuries weakens, yields may rise.

-

If global growth slows, investors may react in ways that push mortgage rates higher.

In short: even if the Fed cuts rates here at home, global forces may pull rates in the opposite direction.

Bottom Line

The Fed’s decision in September will make headlines, but it doesn’t mean mortgage rates will suddenly fall. Rates are shaped by inflation, investor confidence, economic growth, and even global events—all of which carry more weight than a single move by the Fed.

For buyers and sellers in the DC region, this means one thing: plan for mortgage rates to stay higher than we’d all like, at least for the foreseeable future.