Trump Backs Off Firing Fed Chair Powell—For Now

President Trump said Tuesday he plans to let Jerome Powell finish his term as Federal Reserve chair, brushing it off with, “he’s going to be out pretty soon anyway.”

This comes after weeks of Trump hammering Powell for refusing to cut interest rates. Just last week, Trump even floated the idea of firing him, then walked it back by saying he’s “not planning” to—though he didn’t completely rule it out.

Legally, firing Powell would be tricky. The Fed was designed to be independent of political pressure, and trying to remove the chair could trigger a legal fight and shake financial markets.

Still, Trump isn’t letting up. On Tuesday, while taking questions from reporters, he again slammed Powell for being too cautious about cutting rates—something the White House has been pushing for to stimulate the economy.

How Fed Policy Impacts Foreclosures

When the Federal Reserve makes decisions about interest rates, most people immediately think about mortgage rates, home affordability, and whether now is a good time to buy or sell. But there’s another ripple effect that doesn’t get as much attention: foreclosures.

The Fed’s policy decisions—especially whether to raise, cut, or hold rates—play a huge role in how many homeowners fall behind on their mortgages. Here’s how it works:

1. Higher Rates = More Financial Strain for Some Homeowners

When the Fed keeps rates high, mortgage rates typically stay higher too. For most homeowners with fixed-rate mortgages, this isn’t an immediate problem—they’re locked into the historically low rates many grabbed in 2020 and 2021.

But homeowners with adjustable-rate mortgages (ARMs) or those who bought recently at peak prices feel the pressure. If their monthly payments jump and inflation keeps everyday costs high, some start missing payments. Over time, this can push foreclosure rates higher—especially in markets where wages aren’t keeping up.

2. Cutting Rates Too Fast Could Backfire

It might seem like lowering rates would automatically prevent foreclosures, but it’s not that simple.

If the Fed cuts rates too aggressively and inflation spikes again, homeowners face rising costs for food, gas, and utilities. Even if their mortgage stays the same, their overall budget gets tighter, and that financial stress can still lead to missed payments. Powell’s current “wait and see” strategy is designed to prevent that kind of runaway inflation.

3. Equity Is the Safety Net—For Now

One reason foreclosure rates remain historically low is equity. Most homeowners who bought in recent years have seen their property values rise. Even if they’re struggling financially, they can sell before foreclosure and walk away with cash.

But if home prices level off—or worse, start to decline—more people could end up owing more than their home is worth. That’s when foreclosure numbers usually climb.

4. What This Means for Buyers and Investors

If the Fed keeps rates higher for longer, we could see a slow but steady uptick in foreclosures late this year or into 2026, especially in markets where prices are softening.

For buyers, this won’t be like 2008—there’s too much equity in the system—but it could mean more opportunities to buy homes at better prices. For investors, distressed properties might start showing up more frequently, especially in areas where buyers overstretched during the peak of the market.

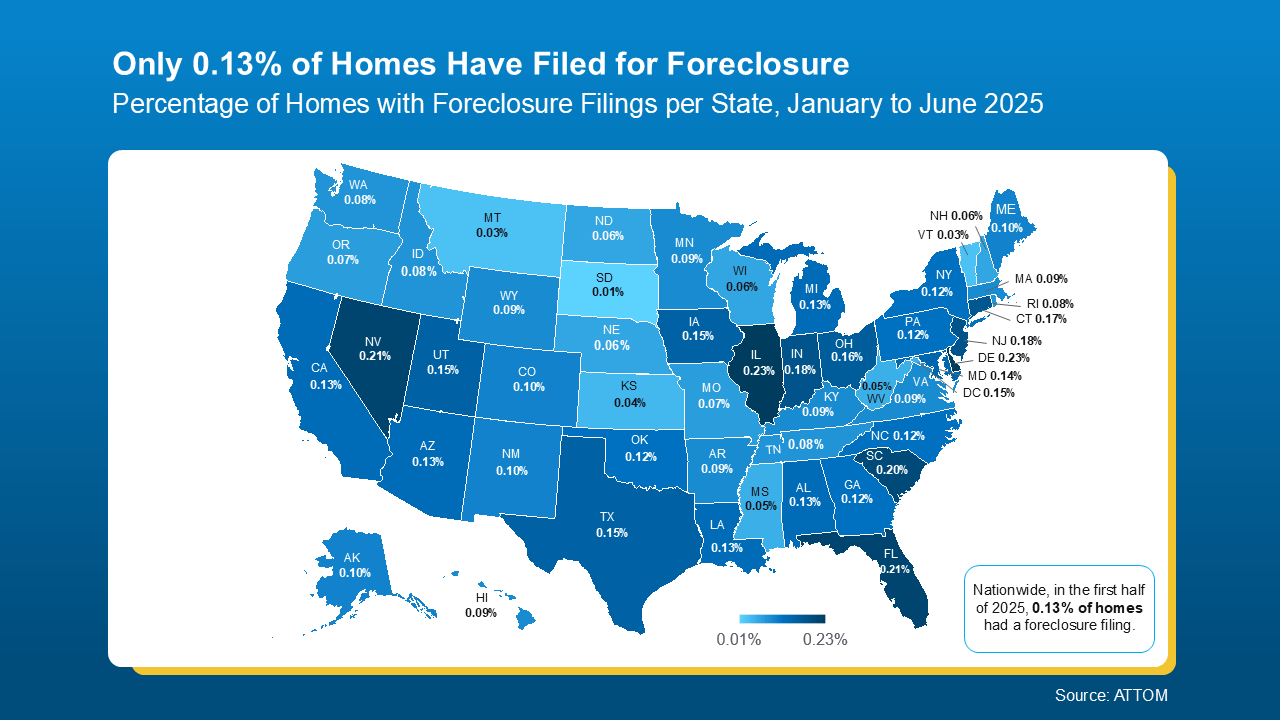

The U.S. Foreclosure Map You Need To See

Foreclosure headlines are making noise again – and they’re designed to stir up fear to get you to read them. But what the data shows is actually happening in the market tells a very different story than what you might be led to believe. So, before you jump to conclusions, it’s important to look at the full picture.

Yes, foreclosure starts are up 7% in the first six months of the year. But zooming out shows that’s nowhere near crisis levels. Here’s why.

Filings Are Still Far Below Crash Levels

Even with the recent uptick, overall foreclosure filings are still very low. In the first half of 2025, just 0.13% of homes had filed for foreclosure. That’s less than 1% of homes in this country. In fact, it’s even far less than that at under a quarter of a percent. That’s a very small fraction of all the homes out there. But like with anything else in real estate, the numbers vary by market.

Here’s the map you need to see that shows how foreclosure rates are lower than you might think, and how they differ by local area:

For context, data from ATTOM shows in the first half of 2025, 1 in every 758 homes nationwide had a foreclosure filing. Thats the 0.13% you can see in the map above. But in 2010, back during the crash? Mortgage News Daily says it was 1 in every 45 homes.

For context, data from ATTOM shows in the first half of 2025, 1 in every 758 homes nationwide had a foreclosure filing. Thats the 0.13% you can see in the map above. But in 2010, back during the crash? Mortgage News Daily says it was 1 in every 45 homes.

Today’s Numbers Don’t Indicate a Market in Trouble

But here’s what everyone remembers…

Leading up to the crash, risky lending practices left homeowners with payments they eventually couldn’t afford. That led to a situation where many homeowners were underwater on their mortgages. When they couldn’t make their payments, they had no choice but to walk away. Foreclosures surged, and the market ultimately crashed.

Today’s housing market is very different. Lending standards are stronger. Homeowners have near record levels of equity. And when someone hits financial trouble, that equity means many people can sell their home rather than face foreclosure. As Rick Sharga, Founder of CJ Patrick Company, explains:

“. . . a significant factor contributing to today’s comparatively low levels of foreclosure activity is that homeowners—including those in foreclosure—possess an unprecedented amount of home equity.”

No one wants to see a homeowner struggle. But if you’re a homeowner facing hardship, talk to your mortgage provider. You may have more options than you think.

The Bottom Line

The Fed isn’t making decisions based on the housing market alone—it’s looking at the entire economy. But every rate decision has a ripple effect on homeowners, and over time, that can influence how many homes end up in foreclosure. For now, foreclosure rates remain low, but if rates stay high and the economy slows, we could see an increase in distressed sales over the next 12 to 18 months.

If you’re a homeowner worried about falling behind—or an investor watching for opportunities—it’s important to stay informed, not just about the real estate market, but about what the Fed is signaling for the economy as a whole.

Recent headlines may not tell the whole story, but the data does. Foreclosure activity remains low by historical standards and is not a sign of another crash.

If you’re simply watching the market and want to understand what’s really going on, or how this impacts the value of your home, let’s connect. I’ll help you separate fact from fear by showing you what the data really says.